Financial services call center outsourcing means delegating customer support operations to specialized external teams trained specifically for banking, insurance, and fintech environments. Unlike general call center outsourcing, financial services outsourcing handles regulated data, identity verification, fraud alerts, and compliance-sensitive transactions—where a single mistake can trigger regulatory violations or customer churn.

The challenge: balancing cost efficiency with security, speed with compliance, and scalability with customer trust. When executed properly, outsourcing absorbs call volume during peak demand, provides 24/7 coverage across time zones, and converts fixed staffing costs into flexible, usage-based pricing.

This guide explains what financial services call center outsourcing actually involves, when it makes strategic sense, and how to select providers who understand the stakes.

Key Takeaways

- Financial services outsourcing requires specialized capabilities beyond basic call handling—including PCI compliance infrastructure, identity verification workflows, fraud detection protocols, and audit-ready call recording with multi-year retention.

- Financial institutions outsource to absorb unpredictable call spikes (fraud alerts, claims surges, product launches), provide round-the-clock support without triple-shift costs, and convert fixed staffing expenses into variable, demand-based pricing.

- PCI DSS certification, encrypted call storage, role-based system access, and agents trained on financial products and verification procedures are baseline requirements—not optional upgrades.

- Outsourcing enables rapid scaling during seasonal peaks (tax season for credit unions, claims season for insurers, trading volatility for crypto exchanges) without long-term staffing commitments or severance costs when volume normalizes.

- Well-executed outsourcing reduces wait times during high-volume periods, maintains consistent service quality through documented workflows, and preserves customer trust through proper training and security controls.

- Provider selection requires verifying financial services experience (case studies, client references), confirmed compliance certifications (PCI AOC, SOC 2 reports), and operational transparency (real-time reporting, clear SLAs, documented security protocols).

What Is Financial Services Call Center Outsourcing?

Financial services call center outsourcing transfers customer support operations to specialized external teams trained in banking products, insurance policies, payment processing, and identity verification procedures. Unlike general customer service outsourcing, agents in financial services environments work within strict regulatory frameworks—handling account credentials, transaction disputes, fraud investigations, and compliance-sensitive conversations where errors carry legal and financial consequences.

The distinction matters because financial services call centers operate under regulatory scrutiny that doesn’t apply to general customer support. Agents access account balances, process payments, verify identities, and handle fraud alerts—activities that require PCI compliance infrastructure, background-checked staff, encrypted systems, and audit trails. Training extends beyond customer service scripts to include financial product knowledge, verification protocols, and regulatory requirements specific to banking, insurance, or fintech operations.

Structurally, this falls under Business Process Outsourcing (BPO)—delegating operational execution while retaining oversight and control. For financial institutions, customer support is operationally critical but doesn’t require in-house management. The value proposition: access trained agents and compliance-ready infrastructure without building and maintaining your own call center operation.

Typical interactions include account balance inquiries, transaction disputes, payment confirmations, loan status updates, insurance claims intake, policy changes, and fraud alert verification. These represent high-volume, standardized workflows where consistency and accuracy matter more than specialized expertise—making them ideal candidates for trained outsourced teams using documented procedures.

Here’s how financial services call centers differ from general call centers:

| Aspect | Financial Services Call Centers | General Call Centers |

|---|---|---|

| Data handled | Financial and personal data | General customer data |

| Compliance | Regulated standards (PCI, privacy laws) | Limited or none |

| Agent training | Financial products and verification | Basic customer service |

| Risk level | High | Low to moderate |

For retail banks and credit unions, outsourced agents often manage inbound support for everyday banking needs. Insurance companies rely on them for claims intake and policy servicing. Fintechs use outsourcing to scale fast without building large in-house teams.

A real example: during a fraud spike, an outsourced financial call center can add trained agents within days. Internal teams usually can’t scale that fast without sacrificing service quality.

Why Financial Institutions Outsource Call Center Services

Financial institutions face operational pressure that makes in-house call centers increasingly impractical. Customer expectations include sub-minute wait times, 24/7 availability, and seamless support across channels—requirements that demand significant infrastructure and staffing investment. Meanwhile, call volume fluctuates unpredictably based on external factors: fraud alerts spike during security incidents, insurance claims surge after disasters, and fintech KYC inquiries multiply during product launches or market volatility.

Outsourcing addresses these operational challenges through flexible staffing models, compliance-ready infrastructure, and specialized expertise that would be expensive to replicate internally:

- 24/7 availability without triple-shift overhead: Card fraud, account lockouts, and payment failures don’t respect business hours. International fintech customers expect support across time zones. Running three internal shifts means tripling management complexity, increasing burnout risk, and paying premium rates for night and weekend coverage—costs that remain fixed even during low-volume hours.

- Absorbing unpredictable volume surges: A fraud alert system triggers 5,000 calls in two hours. Tax season doubles credit union inquiries. Natural disasters generate 10,000+ insurance claims within 48 hours. Internal teams can’t flex this rapidly—hiring requires 6-8 weeks, training adds another 3-4 weeks, and by the time new agents reach productivity, the crisis has already damaged customer satisfaction.

- Converting fixed costs to variable expenses: Internal call centers carry fixed overhead regardless of call volume—salaries, benefits, management, infrastructure, and technology costs remain constant whether you handle 10,000 or 100,000 calls monthly. Outsourcing shifts to usage-based pricing where costs scale proportionally with actual demand, eliminating wasted capacity during slow periods and avoiding emergency overtime during peaks.

- Accessing compliance infrastructure without building it: PCI DSS certification, SOC 2 audits, call recording retention, and agent background checks require dedicated compliance staff, security systems, and ongoing monitoring. For institutions without existing call center operations, this represents $50K-$100K annually in overhead before handling a single customer call. Established outsourcing providers include compliance infrastructure in their base offering.

- Freeing internal teams for strategic work: Account balance inquiries, transaction confirmations, and password resets are operationally necessary but don’t require specialized financial expertise. Outsourcing handles high-volume standardized interactions, allowing internal staff to focus on complex cases, escalations, fraud investigations, and customer relationships that benefit from institutional knowledge.

Practical example: A regional credit union handles 2,000 calls monthly during normal periods, rising to 8,000 during tax season (January-April) when members have questions about tax documents, IRA contributions, and loan interest statements.

Without outsourcing: Staff for peak volume = 75% wasted capacity for 8 months. Staff for average = 15-minute wait times and customer complaints during tax season.

With outsourcing: Maintain core team of 5 internal agents year-round for complex cases. Add 15 outsourced agents January-April for standardized inquiries. Result: consistent service quality during peaks, no idle agents during slow months, and 40% lower total staffing costs.

Outsourcing is not about replacing internal teams. It’s about absorbing volume and handling standardized interactions efficiently while internal staff manage complex or escalated cases.

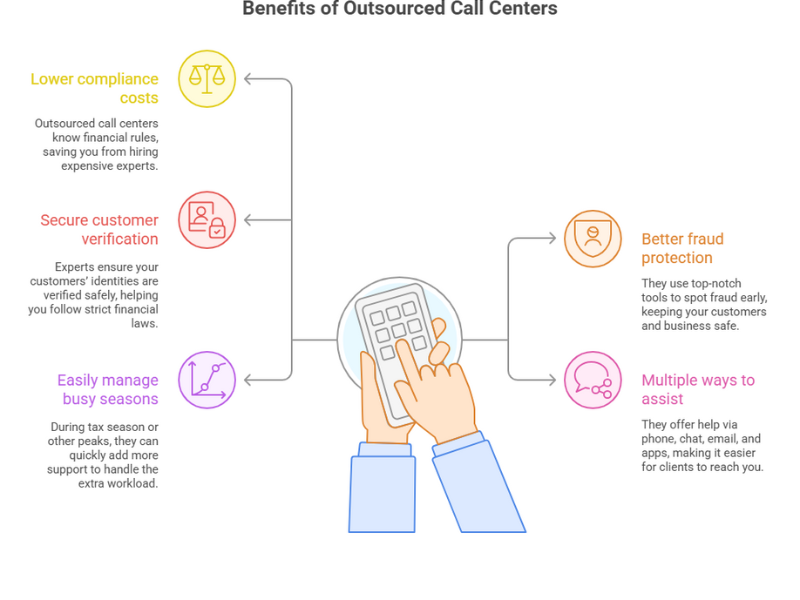

Key Benefits of Financial Services Call Center Outsourcing

Cost Control and Operational Efficiency

In-house call center operations carry substantial hidden costs beyond agent salaries. Infrastructure includes phone systems, CRM software, quality monitoring tools, and workspace. Management requires supervisors, QA specialists, and trainers. Technology needs ongoing maintenance, updates, and integration work. Turnover—typically 20-30% annually in call centers—means constant recruiting, onboarding, and retraining expenses.

Outsourcing fundamentally changes call center economics by converting fixed overhead into variable, usage-based costs. Instead of maintaining permanent capacity for peak demand—leaving agents idle during slow periods—you pay only for actual call volume. During seasonal lulls, costs drop proportionally. During unexpected surges, capacity scales without emergency hiring.

Key efficiency gains include:

- Reduced hiring and onboarding costs.

- No need to invest in call center infrastructure.

- Faster time-to-productivity with trained agents.

- Easier budgeting with clear pricing models.

For smaller financial institutions and fintech startups, outsourcing provides access to enterprise-grade infrastructure, compliance certifications, and trained agents without the capital investment and overhead that larger competitors can absorb. A 15-person community bank can offer the same 24/7 support quality as national banks—without maintaining a 45-person internal call center team.

Compliance and Data Security Support

Data security and regulatory compliance are non-negotiable in financial services call centers. Every call potentially involves account credentials, social security numbers, payment card data, or personally identifiable information. A single breach triggers regulatory investigations, substantial fines, legal liability, and customer trust damage that outlasts the immediate incident. Reputable providers build compliance into operational design rather than treating it as an add-on. For fintech and crypto platforms, proper crypto KYC verification is critical to secure compliance and prevent fraud.

PCI DSS (Payment Card Industry Data Security Standard) certification is the minimum threshold for any provider handling payment-related calls. PCI compliance requires network segmentation, encryption, access controls, regular security testing, and documented policies—independently verified through annual audits. Beyond PCI, strong providers enforce role-based access controls (agents only access data necessary for their function), maintain encrypted call recordings with searchable transcripts, and generate audit trails tracking all system access and data modifications.

What to expect:

-

Compliance-ready operations include:

Multi-factor authentication and identity verification: Documented procedures for confirming customer identity before accessing account information, using knowledge-based questions, one-time codes, or biometric verification depending on risk level.

Least-privilege access controls: Agents receive system access only for their specific role and client accounts. Supervisors and QA staff have appropriately elevated permissions. All access is logged and regularly audited.

Encrypted recording and retention: All calls recorded, encrypted at rest and in transit, with configurable retention periods (typically 1-7 years based on regulatory requirements). Recordings include searchable transcripts for audit and dispute resolution.

Regular compliance audits: Annual PCI audits by qualified security assessors (QSAs), quarterly vulnerability scans, and internal compliance reviews with documented findings and remediation.

Documented incident response: Written procedures for data breaches, system compromises, or compliance violations—including notification timelines, containment steps, and remediation processes.

Critical verification step: Request actual compliance documentation during vendor selection—not promises about future certification. Specifically ask for: current PCI AOC (Attestation of Compliance), latest SOC 2 Type II report, and documented security policies. Providers unwilling to share this information are either non-compliant or unwilling to demonstrate compliance, both disqualifying factors for financial services work.

Checklist to verify compliance readiness:

- Documented security policies.

- Verified PCI compliance status.

- Agent background checks.

- Encrypted systems and recordings.

Scalability and Flexibility

Financial services call volume fluctuates based on external factors largely outside institutional control: regulatory changes trigger verification calls, market volatility drives trading inquiries, fraud incidents spike alert volume, and seasonal patterns (tax season, claims season, enrollment periods) create predictable but dramatic volume swings. Internal teams sized for average demand struggle during peaks; teams sized for peak demand sit idle during normal periods. Outsourcing resolves this mismatch by scaling capacity to match actual demand.

Benefits include:

- Rapid ramp-up during seasonal peaks.

- Easy scale-down when volume drops.

- No permanent headcount commitments.

This operational flexibility proves especially valuable during:

- Insurance claims seasons: Hurricane season, wildfire season, or winter storm periods when claims volume increases 200-400% temporarily

- Banking regulatory changes: New disclosure requirements, updated verification procedures, or policy modifications that generate customer questions

- Fintech product launches: New features, market expansions, or partnership announcements that drive support inquiries

- Fraud incidents: Security breaches, phishing campaigns, or payment processor issues that trigger verification call spikes

Improved Customer Experience and Trust

Customer experience quality in outsourced operations depends entirely on training depth, process documentation, and technology integration. Poorly executed outsourcing—undertrained agents reading generic scripts without account context—damages customer relationships. Well-executed outsourcing—trained agents with CRM access, documented workflows, and quality monitoring—maintains or improves service quality while handling higher volume.

Key impacts:

- Shorter wait times during high volume.

- Consistent answers using approved scripts and CRM data.

- Personalized service through account history access.

- Multilingual support for diverse customer bases.

Practical example: A Texas-based credit union serves both English and Spanish-speaking communities. Before outsourcing, Spanish-speaking customers waited for the one bilingual internal agent or struggled through English conversations. Average handle time for Spanish calls: 8.5 minutes. After adding Spanish-speaking outsourced agents, average handle time dropped to 5.2 minutes, first-call resolution increased from 72% to 89%, and customer satisfaction scores for Spanish-language support rose 23 points—while costs remained lower than hiring multiple full-time bilingual internal agents.

Common Financial Services Outsourced to Call Centers

Banking and Credit Union Customer Support

Outsourced agents handle balance checks, transaction questions, card issues, and branch information. These tasks are repetitive and well-suited to trained external teams.

This reduces internal workload while maintaining service levels.

Insurance Customer Service and Claims Handling

Call centers manage claims intake, policy updates, and coverage questions. Seasonal claim spikes make outsourcing especially valuable.

Agents follow structured workflows to ensure accuracy and consistency.

Loan, Mortgage, and Payment Support

Customers often call for status updates, payment questions, and document confirmation. Outsourcing handles volume efficiently while freeing loan officers for complex cases.

Fraud Prevention and Account Verification

Outsourced teams support identity verification and fraud alerts using defined scripts and tools. Proper training is critical to avoid errors.

These teams act as the first response, escalating confirmed risks internally.

Features to Expect from a Financial Services Call Center Provider

- Omnichannel support across phone, chat, and email.

- Multilingual call routing based on customer preference.

- CRM integration for real-time account access.

- AI-assisted call monitoring for quality control.

- Clear SLAs for response time and availability.

How to Choose a Financial Services Call Center Outsourcing Partner

Industry Experience and Financial Expertise

Financial services call center work requires specialized domain knowledge that general customer service experience doesn’t provide. Agents need to understand financial products (checking accounts, credit cards, investment accounts, insurance policies), industry terminology (APR, deductibles, underwriting, KYC), regulatory requirements (required disclosures, verification procedures, documentation standards), and risk awareness (fraud indicators, suspicious activity, identity theft patterns). Providers lacking this expertise produce agents who give incorrect information, miss fraud signals, or create compliance violations.

Security Standards and Compliance Capabilities

Security and compliance function as operational foundations in financial services call centers, not features added after basic operations are established. Infrastructure design, agent workflows, system access controls, and monitoring procedures must incorporate security from initial setup. Retrofitting security into existing operations introduces gaps, inconsistencies, and compliance failures.

Evaluate:

- Certifications and audit history.

- Data handling and access controls.

- Incident response plans.

Critical warning sign: Providers who respond to security questions with vague assurances (“we take security very seriously”) rather than specific documentation and procedures either lack proper controls or refuse transparency. Both scenarios disqualify them for financial services work where you share liability for their security failures.

Technology, Reporting, and Transparency

Strong providers integrate with existing CRM systems and offer clear reporting. Choosing the right fintech customer service software is equally important, as it enables real-time data access, automation, and seamless customer interactions across channels.

You should see metrics on call volume, resolution time, and quality scores. Transparency builds trust and control.

Location and Staffing Model

Onshore teams offer cultural alignment and time zone coverage. Offshore teams offer cost advantages.

Choose based on customer expectations, language needs, and risk tolerance.

Risks and Considerations in Financial Call Center Outsourcing

- Data privacy risks increase with weak controls.

- Brand voice can suffer without proper training.

- Over-dependence on one vendor creates risk.

- Pilot programs reduce exposure before full rollout.

Who Should Consider Financial Services Call Center Outsourcing?

- Retail banks and credit unions with growing call volume.

- Insurance companies facing seasonal demand.

- Fintech startups scaling faster than internal teams.

- Financial businesses needing 24/7 customer support.

FAQ

Is financial services call center outsourcing secure?

Yes, when providers follow strict security standards and compliance requirements. Always verify certifications and audit processes.

What types of financial companies use outsourced call centers?

Banks, credit unions, insurance firms, and fintechs commonly use them for customer support and verification.

Can outsourced agents handle sensitive financial data?

Trained agents with proper access controls can handle sensitive data safely under defined procedures.

How fast can an outsourced call center scale?

Most providers can add trained agents within days or weeks, depending on demand and complexity.

Is outsourcing suitable for small financial businesses?

Yes. It helps smaller teams access professional support without heavy upfront investment.

Conclusion & Call to Action

Financial services call center outsourcing solves specific operational challenges when executed properly: absorbing unpredictable volume fluctuations, providing 24/7 coverage without triple-shift overhead, converting fixed staffing costs into variable expenses, and accessing compliance infrastructure without building it internally.

Success requires selecting providers with demonstrated financial services expertise, verified compliance certifications, transparent security practices, and technology integration capabilities. The wrong provider—lacking domain knowledge, compliance rigor, or operational transparency—creates more problems than they solve through incorrect customer information, security vulnerabilities, or poor service quality.

Outsourcing makes strategic sense when:

- Call volume fluctuates significantly based on seasonal patterns, product launches, or external events

- Customer expectations require 24/7 availability your internal team can’t sustainably provide

- Compliance and security requirements demand infrastructure investment disproportionate to your call volume

- Speed matters—you need operational capacity in days or weeks, not months

- Budget constraints favor variable costs over fixed overhead

Evaluate your current situation: If wait times regularly exceed 5 minutes, seasonal peaks overwhelm internal teams, you lack 24/7 coverage, or upcoming changes (regulatory, product, market) will increase call volume, outsourcing deserves serious consideration.

The right partner doesn’t replace your internal team—they complement it by handling standardized, high-volume interactions while your staff focuses on complex cases, escalations, and customer relationships benefiting from institutional knowledge.

FAQs

What is financial services call center outsourcing?

Financial services call center outsourcing involves delegating customer support tasks to specialized external providers. These providers handle activities such as account inquiries, loan applications, claims processing, and fraud prevention, ensuring secure and efficient service tailored to the financial industry.

Why should financial institutions outsource call center services?

Outsourcing helps financial institutions offer 24/7 support, manage peak seasons, reduce operational costs, and ensure regulatory compliance. It also improves customer experiences by providing faster response times, multilingual support, and personalized interactions.

What types of services can be outsourced in financial call centers?

Common services include banking customer support, insurance claims handling, loan and mortgage inquiries, fraud detection, and account verification. Additional tasks like appointment scheduling and technical support can also be outsourced.

How do outsourced call centers protect customer data?

Outsourced call centers use strict security protocols, including PCI compliance and ISO certifications, to safeguard customer data. They implement encryption, monitoring tools, and identity verification to ensure privacy and prevent breaches.

What are the benefits of outsourcing financial call center services?

Benefits include lower costs, scalability, compliance support, improved customer satisfaction, access to trained agents, and omnichannel communication. Outsourcing also frees internal teams to focus on critical business functions.

How should I choose the right outsourcing partner for the financial industry?

Look for providers with expertise in financial services, proven regulatory compliance, advanced technology integrations like CRM systems, and a strong track record. Evaluate their scalability, multilingual support, and ability to align with your brand voice.

Is outsourcing suitable for small financial businesses?

Yes, outsourcing can benefit small financial businesses by providing cost-effective access to specialized agents, reducing staffing expenses, and offering scalable solutions to meet fluctuating customer demands.

Are there risks involved in financial call center outsourcing?

Risks include data privacy concerns, dependency on external providers, and potential misalignment with your brand voice. Mitigating these risks requires thorough vetting, clear SLAs, and ongoing performance monitoring.

Read more:

Customer Experience Principles: 7 Practical Rules to Improve CX

Customer Experience Transformation: Practical Strategies

More in Industry

View all →

What Is an Ecommerce Call Center?

An ecommerce call center helps online stores handle customer questions before and after purchase, faster and with more consistency. If your team is dealing with order issues, returns, shipping questions, checkout problems, or rising support volume, the right setup can protect sales, improve customer satisfaction, and make scaling easier without creating support chaos. What Is an Ecommerce Call Center? Simple…

SaaS Customer Support Outsourcing: Top Partners, Benefits, and How to Choose

SaaS support gets harder as ticket volume grows faster than your team can scale. If you’re exploring SaaS customer support outsourcing, this guide shows what it is, when it makes sense, how it works, what risks to watch, how pricing usually works, and which providers are worth shortlisting. The goal is simple: help you choose a partner that improves customer…

9 Best Voice Chat Apps for Gaming (2026 Comparison)

If your in-game voice chat is cutting out, teammates can't hear your callouts, or your squad is on different platforms, you need better call software for gaming. This guide cuts through the noise: what "call software gaming" actually is, how to choose it, and the best tools for real gameplay needs. Why Voice Chat Matters for Modern Gamers “Call software…